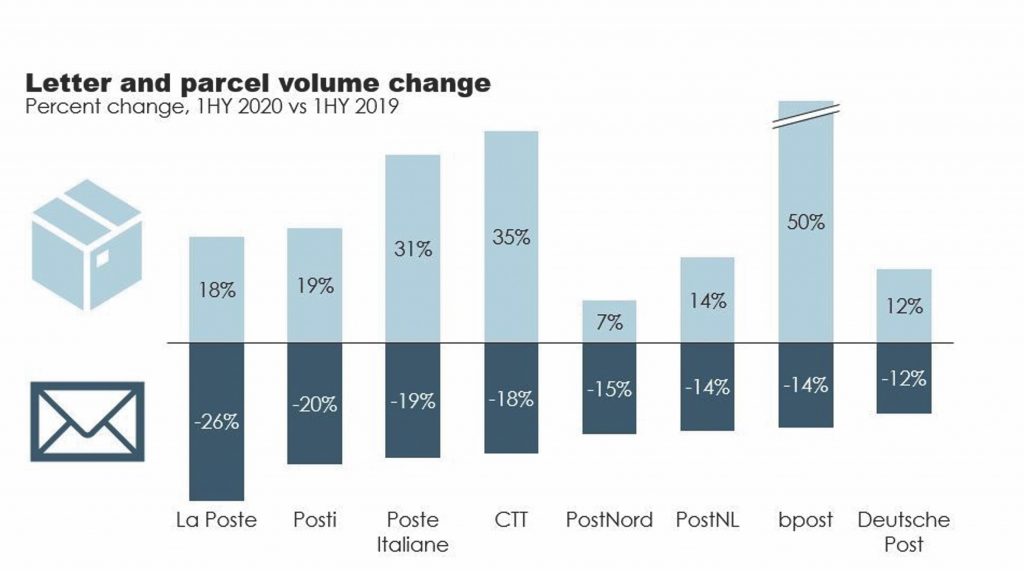

Since the world was hit by the Covid-19 pandemic, parcel volumes have significantly increased around the world. For example, in France volumes shot up around 50% year-on-year and have remained 20-30% higher than 2019 since the first lockdown. Spain had already experienced a doubling of B2C parcel volumes from 2018 to 2020, which was pushed even higher by Covid-19. The chart (right) shows the impact on parcel and letter volumes – though this includes the three months January-March, which were prior to most of the major lockdowns.

Sudden spikes in volume are hard to manage, but surely the growth of parcel volumes should be good news for parcel carriers? Unfortunately, it’s becoming clear that the industry as a whole is experiencing diminishing returns as parcel volumes grow, even before we account for the exceptional circumstances of Covid-19.

What the research says

Pitney Bowes’ global parcel index for 2019 was published in October 2020 and revealed that while volumes and revenues have both been growing, volumes are growing much more quickly. Volume grew nearly 18% between 2018 and 2019, but revenue only rose by 11% in that time. Incidentally, the report also forecast that by 2026, parcel volumes globally will rise to double the 103 billion shipped in 2019. Of course that growth will not be evenly distributed, but it’s a useful exercise for leaders of posts and parcel carriers to imagine how their businesses will deal with double their current volumes in such a short time period.

The numbers tell us we’re entering a period of diminishing returns, where doing more business will eventually start to hurt profitability rather than help it. To tackle that, carriers will need to transform the basic economics of their model. Doubling capacity by building new infrastructure and driving more miles won’t work – it’s unaffordable in the short term and the horizon for those investments breaking even will keep moving further away as volumes rise faster while revenues and margins remain tight.

A new approach

There will be different responses in different markets. In the USA, for example, parcel carriers like FedEx and UPS already charge an additional fee or residential surcharge for package delivery to residential addresses, because these deliveries are economically unsustainable otherwise. We could well see these charges rising and more carriers may be interested in adopting this model, if the market will allow them to. However, in price-sensitive markets like the UK this is unlikely to be accepted, as introducing a surcharge will simply make your service cost more than a like-for-like competitor.

That leaves many carriers with few ways to sustain their current home delivery proposition, at least as it exists today, with a vast majority of volume delivered to-door. The key for these businesses will be to drive increased adoption of out-of-home delivery models, which allow for consolidation and the consequent benefits to efficiency and unit economics.

One effect of the pandemic-induced volume surge was that it shocked parcel carriers and postal operators into speeding up their plans for consolidation and out-of-home delivery. Businesses that previously talked of 5- to 10-year plans have started talking about deployments happening in months. Interest in PUDO formats like lockers has continued to grow, driven by explosive growth in usage.

According to Asta Sungailiene, CEO of Lithuanian Post, locker use has increased by over 200% in the country during Covid, and the post is now doing locker deliveries up to four times per day. And we’ve heard similar stories in China, Poland and Spain – all markets where lockers make up a large proportion of PUDO locations. However, as restrictions eventually ease and something like normality prevails, it will be important to bring consumers back to parcel shops as well. Lockers are part of the consolidation mix, but these alone will not offer the capacity or rapid scalability that parcel shop or over-the-counter PUDO can.

Challenges abound, but increasing consolidation is the path parcel carriers will have to tread to remain economically viable – and ecologically and societally more sustainable to boot.