New research shows that Poland’s parcels market is growing at a staggering rate, with players such as InPost driving innovation in one of Europe’s most dynamic last-mile markets. Analysis from Marek Różycki (Last Mile Experts).

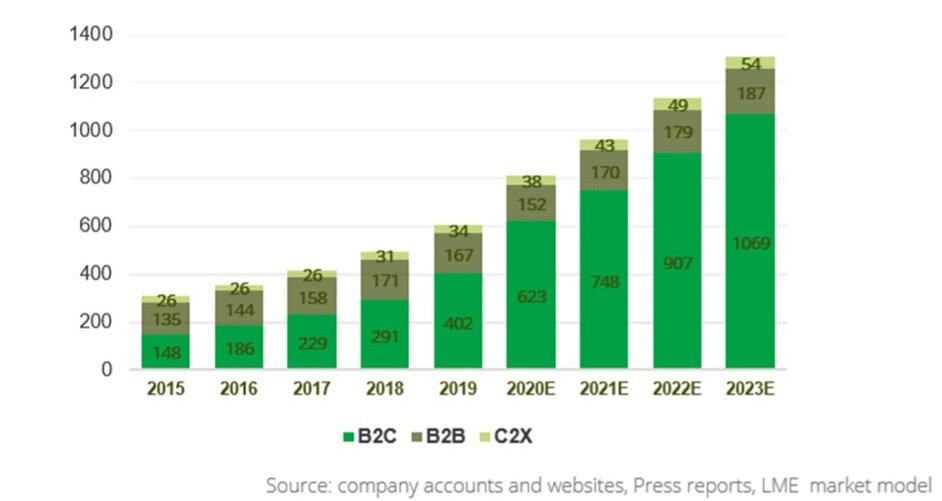

Poland’s parcels market could reach 1.31 billion parcels by 2023, according to new research. The Polish CEP report 2021 from Last Mile Experts shows that new players such as InPost are starting to dominate the market, at the expense of legacy carriers such as Polish Post.

The rapid growth of e-commerce has powered innovation in B2C parcel delivery, resulting in Poland being a leader in out-of-home (OOH) delivery – in particular with parcel lockers as well as pick-up/drop-off points (PUDOs).

But growth alone hasn’t driven Poland’s leading-edge approach to delivery; the need for capacity, along with the demand from vendors and consignees for ever more consumer-centric and flexible last-mile services, has led to Poland being one of Europe’s most dynamic markets in the last mile.

The threat of Amazon’s imminent entry into the Polish market has encouraged the key local players, notably InPost, to learn from the e-commerce behemoth, which has helped make this one of the most innovative CEP markets in Europe.

The Polish parcels market reached almost zł10.7bn (US$2.9bn) and 814 million parcels in 2020, following dynamic growth in recent years as economic performance has improved and e-commerce growth has exploded.

We estimate that the Poland parcels market will reach a market value of zł16.2bn (US$4.3bn) and market volume of 1.31 billion parcels in 2023, with B2C clearly the largest segment of the market. B2C parcel growth will reach 72% by 2023 by volume (19.7% CAGR)

Market growth has been most rapid in the out-of-home (OOH) segment. The biggest winners have been InPost, which grew 108% in 2020 and at over 250% CAGR 2015-2020 by volume, and which is now market leader; and Żabka which has come from nowhere to become a leading independent OOH enabler. The key losers are the legacy carriers who have not been able to embrace the demands of the new last mile.

Delivery developments

Leading e-tailers, such as Allegro or, to a lesser degree, Empik, are increasingly getting involved in delivery, especially via subscription delivery models, reflecting the strategic importance of it to their business models. Their large volumes give them significant market power. Amazon’s entry and the development of Alibaba’s business are now just a matter of time. JD.com is not particularly active or visible in the market right now; this may change if Alibaba shows successful development in Poland.

Carriers are investing in improving their systems, and in particular interactive delivery management (IDM), to provide better customer experience for consignees and to improve their operational efficiency and effectiveness. Indeed, new technology is being applied more and more widely throughout carrier operations, from automated sorting and robotics in hubs and depots to use of lockers and parcel robots (robotic lockers).

The traditional hub-and-spoke model remains important, but disruptors and e-grocery players are looking at more localized models allowing for faster delivery times.

Same-day and premium deliveries are set to become the next development as the dominant marketplace, Allegro, pushes its partners to develop new super-fast services. InPost and on a smaller scale Xpress Couriers are at the forefront here.

Market leaders

There are two market leaders, InPost and DPD, who together make up well over half of the Polish CEP market, by volume.

InPost is definitely the one to watch; its dominance in lockers (it now has the largest network in Europe with well over 10,000 machines in Poland alone) is a key competitive advantage.

A number of important independent players such as Żabka and Ruch/PKN Orlen have entered the CEP space in the form of infrastructure players but we expect this to develop to a more complex suite of last-mile services.

Amazon already has 10 large fulfillment centers in Poland and an increasingly large tech team. It has recently posted advertisements for retail roles in Poland and we expect full market entry in 2021. Alibaba is present in the market and is developing fulfillment capability, as is Zalando. The only leading e-commerce players that are absent are eBay, which is arguably the result of its failed attempt to de-throne the incumbent marketplace, Allegro, some 10 years ago, and JD.com.

Allegro has just completed a highly successful IPO and is currently developing its own last-mile competence.

We expect to see continued market growth and more customer-centric services and features being largely a function of (as a result of?):

- Post-Covid e-commerce acceleration and the resulting growth in parcels;

- Entry of Amazon and the development of Alibaba and Allegro’s last-mile offerings;

- Creation of an alternative to InPost’s closed parcel network as a result of a consolidation of efforts by all of the carriers unable to leverage InPost’s network;

- Consolidation of InPost into the Hermes network (resulting from Advent’s acquisition of a major stake there) subject only to the results of InPost investment process, which is currently underway;

- Continued decline of the position of the postal incumbent unless the government takes steps to protect its position with anti-competitive regulatory or fiscal measures;

- Development of startups dealing mainly with same-day deliveries; and

- Further development of courier brokers toward IT solutions integrating multiple forms of delivery and opening physical PUDO points.

However we look at it, Poland has become one of the fastest growing and most innovative markets in Europe. It is not only a beacon for the other markets in its region but also for many West European markets that have been slower to accept change, especially in the increasingly important area of locker delivery.

The Last Mile Experts Polish CEP report 2021 is available. This 51-page document is jam-packed with the latest data and covers the period from 2015 up to the present and with forecasts to 2023. The report includes historical and forecast market volumes, values, delivery channels and service type, followed by market overview and trends. Contact info@lmexpert.com for more information.