Interact Analysis’s new report on the future of warehouse automation casts light on some important post-Covid-19 developments in the sector. In earlier insights, we have discussed the impact of the likely long-term behavioral change in consumer habits which the coronavirus will cause, most notably in the field of e-commerce, and the likely impact on warehouse automation that this would have. Our analysts have now gathered a bank of data which we have used in our report to give an informed analysis of the current performance of, and likely short-term prospects for, the main players in the warehouse automation sector.

Overall market forecast

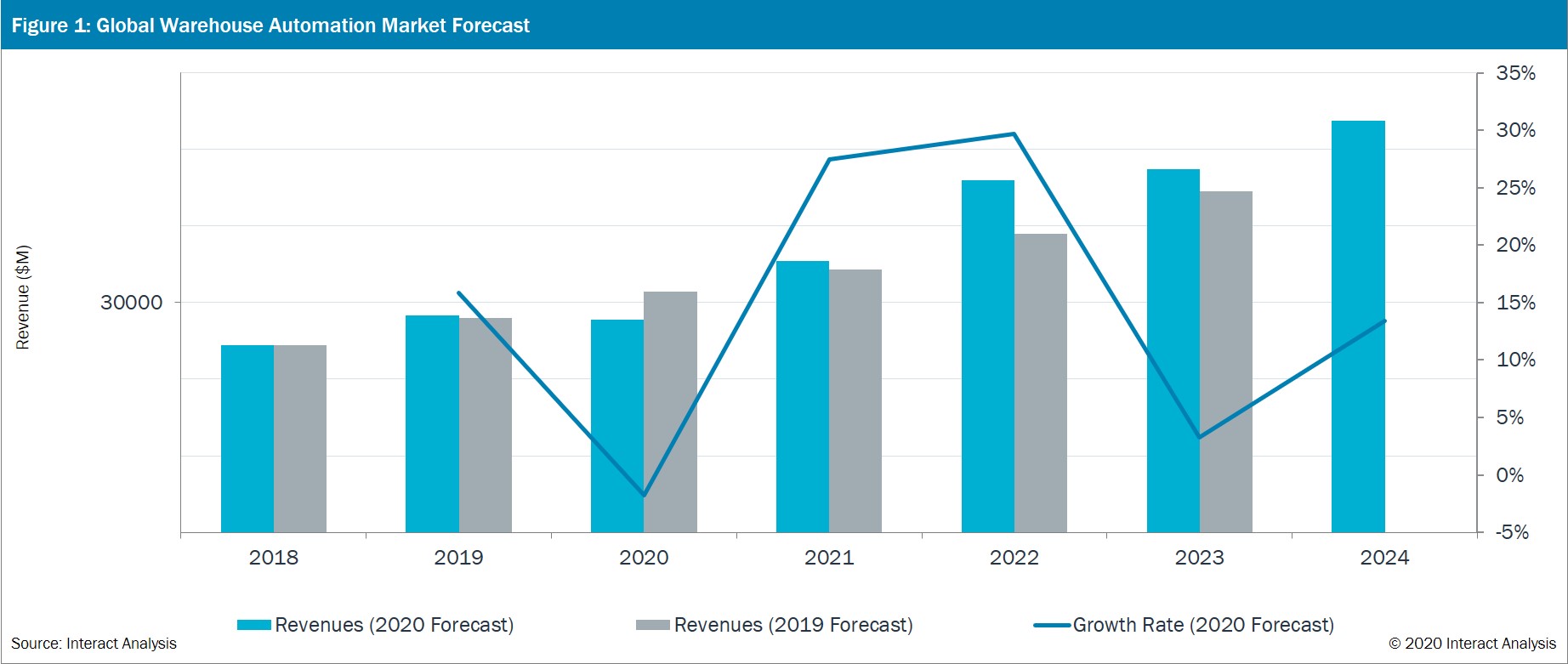

Two distinct sets of figures come into play here: revenues and order intake. Revenues are recognized only when a project is completed, which may be several months or even a year after the order was initially received. Meanwhile, order intake reflects current orders. Order intake is the more relevant to the here and now – and in particular, it sheds light on how Covid has impacted the warehouse automation sector. Our detailed figures for both categories – historical, current and projected – describe overall a sector which is in strong health, notwithstanding the trials caused by the Covid-19 pandemic, which is boosting some areas and causing short-term difficulties for others.

In 2020, we forecast that the total revenue for the global warehouse automation market will decrease by US$500m. And our predictions for the severity of this Covid-related decline have decreased compared with our initial assumptions, which were based on our surveys with warehouse automation providers back in March, April and May. Our data covers the period 2018-2024, and the year 2020 is the only year where there is a reduction in revenue, and it is a relatively small dip, compared with the significant year-on-year increases in the rest of the timeframe.

As can be seen in the graph below [Figure1], we predict big market growth again in 2021 as many project completion dates have been pushed out from 2020 to 2021. This is because warehouse automation companies are now running at full capacity and are rushing to grow their own capabilities to match – as evidenced by the hiring spree that many warehouse automation companies are on, such as Dematic which is currently hiring 1,000 new people. The combined effect of a spike in order intake and projects being pushed out to 2021 will result in a lot of projects being pushed back until 2022. We don’t expect the market to come into equilibrium, or return to ‘normal’ until 2023 – which is why the growth rate for 2023 seems ‘lower’ (in our view it’s not really ‘lower’, it’s just a product of 2021 and 2022 being artificially high).

While revenues are forecast to decline slightly in 2020, order intake is forecast to grow significantly. Orders increased by US$2.5bn in 2020 and are forecast to grow by much larger increments in the coming years. We predict the overall CAGR of the global warehouse automation market will increase by 11.9% in the period 2019-2024. But that figure masks some significantly higher performances in certain sectors of the industry, one of which we shall highlight shortly.

These increases come as a response to customer demand on the ground, putting particular pressure on the general merchandise, food and beverage, and groceries sectors. The challenge has been a huge increase in online orders, which are far more logistically complex to fulfil than traditional brick-and-mortar sales where, essentially, the customer fulfils their own order in store.

This is particularly challenging for retailers who have nascent omnichannel strategies and may not have full visibility of exactly where their stock is at any given time. Other sectors, such as durable and non-durable manufacturing, and the fashion and apparel industry, saw demand for warehouse automation equipment stall in 2020, as Covid hit the shop floor, and factories closed due to lockdowns; but our forecasts see steady increases in demand from these areas as they recover.

Boom time for the groceries sector

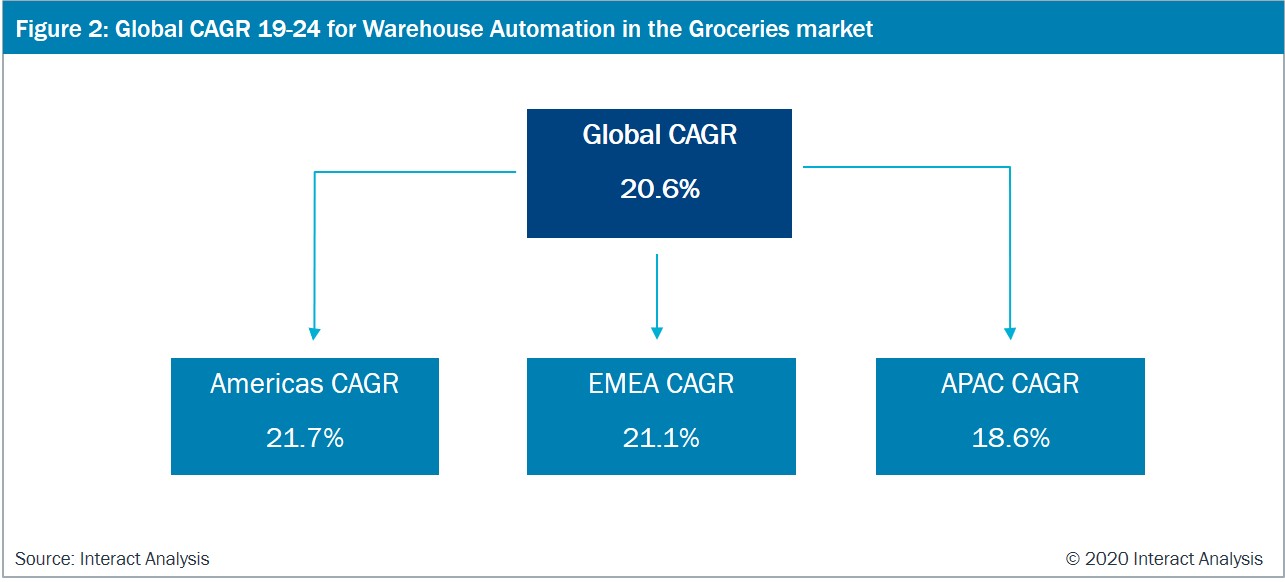

Standing at 20.6%, the predicted 2019-24 CAGR growth of the total order intake for the global groceries sector far outstrips that for other sectors. The figures are fairly consistent across the globe, with EMEA seeing an increase in the CAGR of 21.1%, Americas 21.7%, and APAC 18.6% across the same period. The fact that orders are predicted to grow strongly reflects changing shopping habits as customers stay at home and await the arrival of their groceries in the supermarket van.

As with all sectors, our report goes into intricate detail regarding all facets of the groceries segment, and the impact on the automated equipment market. But one single aspect stands out – the boom in micro-fulfilment centers. Efficient last-mile distribution of fresh groceries is crucial to the success of the online groceries industry, and automated machinery has been recognized as a key player in achieving that success. Our data describes an exponential growth in the demand for automated equipment in micro-fulfilment centers.

Part of the work of any good market research company is the regular analysis and updating of data. Our pre-Covid and post-Covid forecasts for the groceries sector feature in the PDF document accompanying our data and make interesting reading. In the light of the boom in online shopping caused by the virus, we have increased our forecasts of year-on-year sales of automated equipment to the sector by as much as 28%.

Performance of individual automation providers

The top five automated warehouse equipment providers, in terms of 2019 revenues, are: Dematic, Honeywell Intelligrated, SSI Schaefer, Daifuku, and Knapp AG. In 2019, only Knapp AG increased its share of the global market, by a relatively small 0.5%, while the others lost market share. However, Dematic and Honeywell’s order intake for the second quarter of 2020 has seen a dramatic increase, more than any other quarter ever.

Honeywell’s record high order intake of US$1.2bn was up 300% compared with the second quarter in 2019. Dematic’s order intake is up by 100%. Both these companies provide automated machinery to sectors which are forecast to see significant growth – notably the general merchandise and food and beverage industries.

For our upcoming report on warehouse automation, the data for which is now available, we surveyed companies representing 71% of the global market in terms of revenue (excluding China).

To continue the conversation on the warehouse automation market with our lead sector analyst Rueben Scriven, please get in touch: Rueben.Scriven@interactanalysis.com

This article was originally published here.